The COT Report: Reading Market Positioning

The Commitments of Traders (COT) report is a weekly snapshot of who is long and who is short in a futures market — broken down by the kind of trader holding the position. It doesn't tell you where price is going; it tells you how crowded a trade has become, which is a different and often more useful thing. This guide explains how to read positioning in plain English, so the next time a market feels "everyone's already in this," you can actually check.

What the COT report is

Futures markets are one of the few places where you can see, in aggregate, what participants are actually doing — not what they're saying. Regulators require large traders to report their positions, and those positions are published weekly, grouped by trader type. That published summary is the COT report.

Think of it as a periodic headcount of the market. It doesn't name anyone. It just says: as of the reporting date, this many contracts are held long and short by each broad category of participant. The value isn't in any single week's figure — it's in the trend and the extremes.

The trader categories that matter

The report splits participants into groups, and the useful distinction for most people is between two of them:

- Commercials (hedgers). These are businesses with a real-world stake in the physical commodity — producers, processors, merchants. A farmer selling futures to lock in a crop price, an airline hedging fuel. They aren't betting on direction; they're offsetting a physical exposure. Because they're closest to the actual supply and demand, their behaviour is sometimes read as the "smart money" — though that label deserves caution.

- Non-commercials / managed money (speculators). These are funds and large traders positioning for price direction. They have no physical business to hedge; they're there to profit from the move. Their positioning is the clearest read on speculative sentiment.

The tension between these two groups is the heart of the report. Hedgers and speculators are often on opposite sides — by design, because speculators provide the other side of the trade hedgers need.

Why positioning is information

Price tells you where a market is. Positioning tells you how it got there and who's holding the bag.

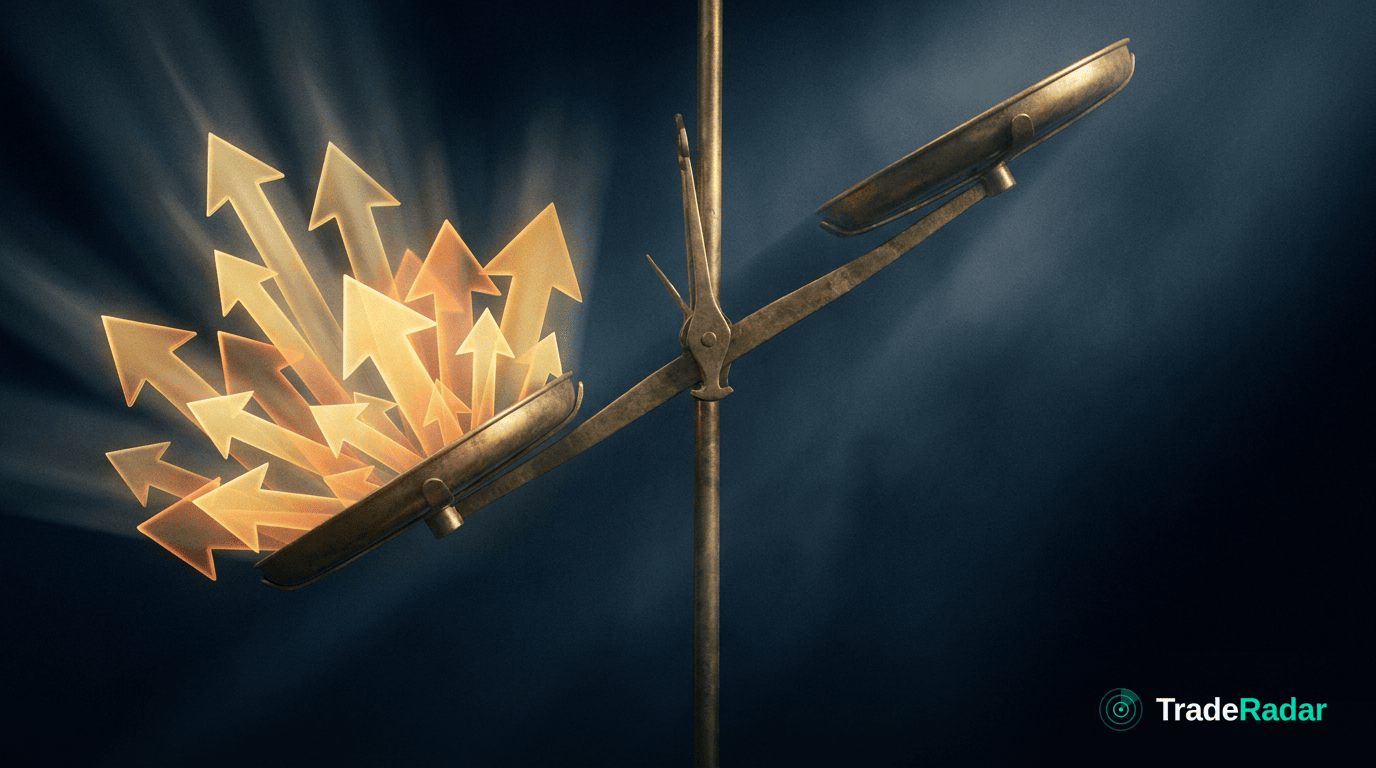

Imagine two markets at the same price. In one, speculators are lightly positioned and have plenty of room to buy. In the other, speculators are already loaded to the gills on the long side. These two markets are not the same, even though the price is identical. The second one has a structural vulnerability the first doesn't — most of the potential buyers have already bought.

This is the core insight: an extreme in positioning means a trade is crowded. And a crowded trade has an asymmetry. When nearly everyone who wants to be long already is, there are few buyers left to push it higher — but plenty of holders who could become sellers if sentiment turns. The fuel for the next move increasingly sits on the opposite side.

Reading extremes, not levels

A raw position number is close to meaningless on its own — markets differ in size and structure. What carries signal is how stretched positioning is relative to its own history.

- A speculative long extreme — funds more net-long than they've typically been — flags a crowded bullish trade. It says sentiment is one-sided, not that a top is in.

- A speculative short extreme — funds heavily net-short — flags a crowded bearish trade, with the same logic reversed.

- A shift in the trend — speculators steadily building or unwinding a position week over week — can show conviction entering or leaving a market before it's obvious in price.

The practical read: extremes mark conditions where a market is vulnerable to a reversal, because it's run out of people to keep pushing the same way. They do not mark timing. A crowded trade can get more crowded for a long time.

What breaks this

Positioning is a genuinely useful lens, and also one of the easiest to over-read. The honest caveats:

- It's a reversal risk gauge, not a timing tool. Extremes can persist and deepen for weeks or months. "Crowded" is not "about to turn." Using positioning as a standalone entry signal is where most people go wrong.

- It's stale by the time you see it. The report reflects a snapshot from earlier in the week, published with a lag. In a fast market, the real positioning may already have shifted.

- Category labels are imperfect. The neat buckets of "hedger" and "speculator" blur at the edges — some traders straddle categories, and the "smart money" reputation of commercials is a generalisation, not a rule.

- Context changes what's extreme. A position level that was extreme in a calm market may be normal in a volatile one. Always compare a market to its own recent range.

- It's one input, not a system. Positioning tells you about fuel and crowding. It says nothing about the fundamentals or the catalyst that might light the fuse.

When positioning is stretched but price keeps trending, that's not the report failing — it's a reminder that crowding sets up a reversal, it doesn't schedule one.

How to actually use this

Treat the COT report as a context layer, not a trigger:

- Check how stretched speculators are versus their own history — crowded or not?

- Watch the direction of the trend — is positioning building or unwinding, and does it agree with price?

- Combine it with a catalyst. Positioning tells you a market is vulnerable; it takes a fundamental shift or a technical break to turn vulnerability into a move.

Seen this way, the question stops being "which way is price going?" and becomes "how crowded is this trade, and who's left to push it?" — a question positioning is genuinely built to answer.

Want positioning sitting right next to price, the curve and the fundamentals — instead of buried in a spreadsheet? That's what TradeRadar is built to do: see the full picture, across assets, in one view.

TradeRadar is decision-support software, not investment advice. Trading involves risk.

Frequently asked

What is the COT report?

The Commitments of Traders report is a weekly, published breakdown of long and short futures positions grouped by trader type. It shows, in aggregate, what market participants are actually doing rather than saying. Its value is in the trend and the extremes over time, not in any single week's number.

What's the difference between commercials and non-commercials?

Commercials are hedgers — businesses with a physical stake in the commodity, like producers and processors, offsetting real-world exposure. Non-commercials, often called managed money, are speculators positioning for price direction with no physical business to hedge. Their positioning is the clearest read on speculative sentiment, and the two groups are often on opposite sides.

Can the COT report predict price direction?

No. It's a gauge of how crowded a trade is, not a timing tool. Extreme positioning flags that a market is vulnerable to a reversal because it's running out of participants to keep pushing the same way — but a crowded trade can stay crowded and get more extreme for a long time before it turns.

Why is positioning useful if it can't time the market?

Because two markets at the same price can be very different underneath. One where speculators are lightly positioned has room to run; one where they're already loaded on one side has a built-in vulnerability. Positioning reveals that hidden asymmetry — where the fuel for the next move actually sits — which price alone can't show.

Related in Macro & Technical

Contango vs Backwardation: What the Futures Curve Tells You

The futures curve tells you how tight a market feels before the flat price does. Here's contango vs backwardation in plain English — and what breaks the read.

Copper: the Growth Barometer They Call Dr Copper

Copper is called Dr Copper because its price reads the health of the global economy. Here's the plain-English mechanism — and what breaks the signal.

EUR/USD and Central-Bank Divergence

EUR/USD is a tug-of-war between two central banks. Here's the plain-English mechanism — how rate divergence drives the pair, and what breaks it.