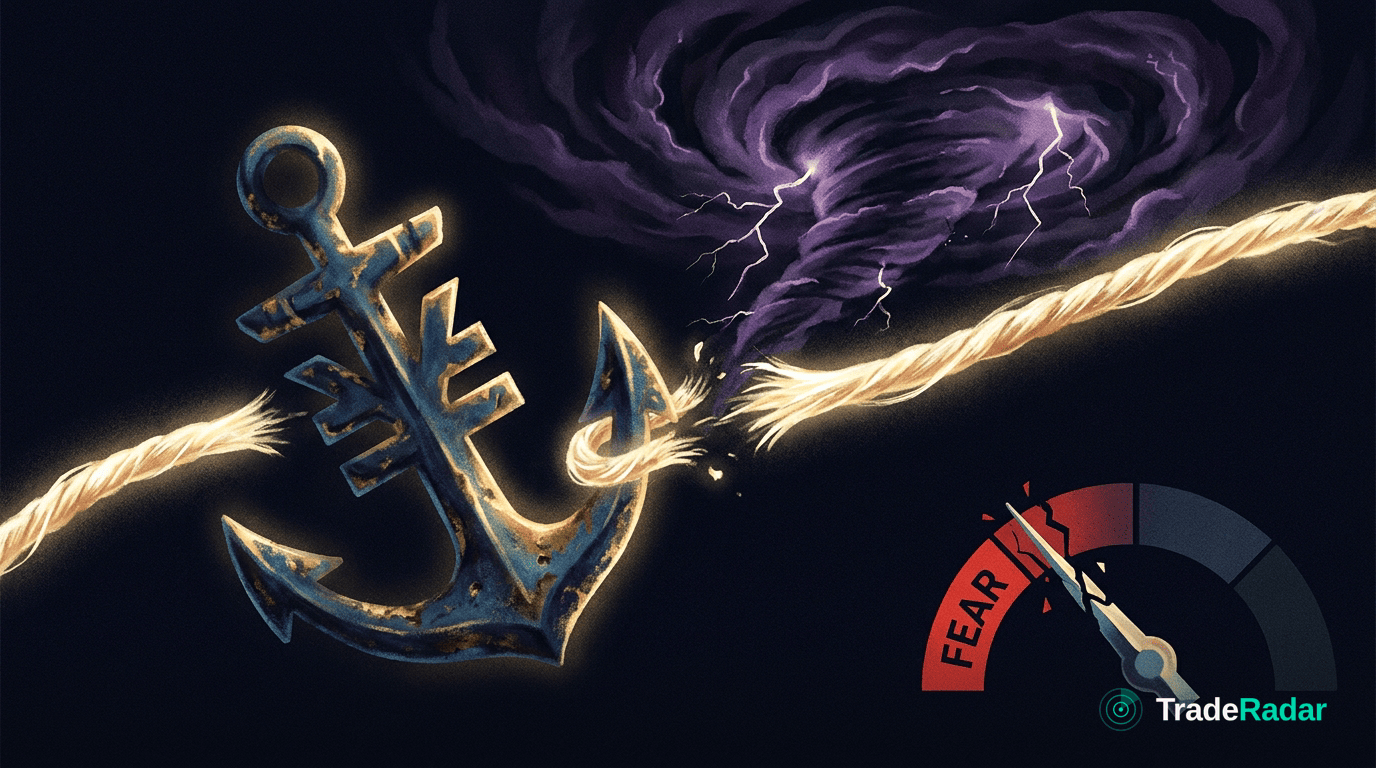

Why the Japanese Yen Is a Risk Barometer (The Carry Trade)

The yen tends to strengthen when markets get scared because it's the currency the world borrows to fund risky bets — and when those bets are unwound, the borrowing is repaid, which buys yen back. In short, the yen behaves like a risk barometer not because Japan is a haven, but because of the mechanics of the carry trade. This guide explains that mechanism in plain English, so a moving yen becomes a signal you can read rather than a currency-market mystery.

Start with the carry trade

The carry trade is one of the oldest ideas in markets: borrow where it's cheap, invest where it pays more, and pocket the difference.

For long stretches, Japan has had among the lowest interest rates in the developed world. That makes the yen an attractive thing to borrow. A trader can borrow yen at a low rate, convert it into a higher-yielding currency or asset, and earn the gap — the "carry" — as long as nothing moves against them.

To do this, they must sell yen to buy the higher-yielding asset. Multiply that across the global financial system — funds, banks, speculators — and you get persistent, structural selling pressure on the yen during calm times. The carry trade is, at its core, a giant short position in the yen.

Why calm markets push the yen down

The carry trade only works while volatility stays low. The profit is the interest-rate gap, which is steady and modest; the risk is that the exchange rate moves and wipes out that gap in a day.

So when markets are calm and trending, the carry trade is comfortable. Money keeps flowing into it, which means more yen keeps being sold. In quiet, risk-on conditions, the yen tends to drift weaker — not because anything is wrong with Japan, but because it's being continuously borrowed and sold to fund positions elsewhere.

This is the baseline. A gently weakening yen is often just the sound of the carry trade running smoothly.

Why fear makes the yen surge

Now flip the regime. Something spooks the market — a shock, a data surprise, a spike in volatility. Risk appetite evaporates. What happens to all those carry positions?

They get unwound, often fast. To close a carry trade you must reverse the original transaction: sell the higher-yielding asset and buy back the yen you borrowed. When fear hits, everyone tries to do this at once.

That synchronised buying is the engine. A wave of carry unwinds means a wave of yen buying, and the yen can surge sharply exactly when equities are falling and volatility is spiking. This is why the yen so often strengthens during selloffs — it's the mechanical footprint of leverage being withdrawn from the system.

The yen isn't reacting to fear emotionally. It's reacting to deleveraging. When the world de-risks, it repays its yen borrowing, and the currency rises.

"Safe haven" is the wrong label

People often call the yen a safe haven, which invites the wrong mental model. A true safe haven is bought because investors want to own it for safety. The yen's strength in a crisis is different: it's bought because it has to be repaid.

The distinction matters because it tells you what to watch. Yen strength is a symptom of risk-off deleveraging, not a vote of confidence in Japan. That's precisely what makes it a useful barometer — it moves with the plumbing of global risk-taking, not with a narrative about one country.

How to read the yen as a signal

You don't need to forecast the yen. You read it as one instrument in the risk orchestra and ask whether it agrees with the others.

- Direction and speed. A slow, quiet drift weaker is consistent with calm, carry-friendly conditions. A sharp, fast surge stronger is the signature of a rush to unwind risk.

- Confirmation with volatility and equities. A yen spike that lines up with a jumping VIX and falling equities is a coherent risk-off signal. All three telling the same story is more convincing than any one alone.

- Divergence as a flag. If equities are calm but the yen is quietly grinding stronger, that can hint at deleveraging under the surface before it shows up elsewhere. Disagreement is worth noticing.

Read this way, the yen is one of the cleaner cross-asset reads on global risk appetite — a currency that reports on the state of leverage in the system.

What breaks the signal

No market relationship is a law, and the yen's carry story has real limits.

- Rate gaps change the setup. The whole trade depends on Japan's rates being low relative to others. As that gap narrows or widens — on either side — the incentive to fund in yen shifts, and the currency's sensitivity to risk-off episodes changes with it.

- Policy can overwhelm it. Central-bank action, currency intervention, or a shift in monetary regime can move the yen for domestic reasons that swamp the carry signal entirely.

- Positioning matters. The yen's crisis surge is powered by an existing pile of carry positions to unwind. When that positioning is light, an unwind has less fuel and the reaction is muted.

- It's a barometer, not a forecast. The yen reflects the state of risk appetite; it doesn't predict what causes the next shock or when.

When the yen sends a signal that other evidence flatly contradicts, that tension is itself information — it usually means either the carry positioning is unusually light, or a domestic policy force is in control. Noticing the disagreement is part of using the yen well.

The one-line takeaway

The yen strengthens in a crisis because the world repays what it borrowed, not because it's running to safety. Read a sharp yen surge as the sound of deleveraging — and as one of the cleaner cross-asset reads on global risk appetite.

Want the whole board this way — every market with its drivers, not just its price? That's what TradeRadar is built to do.

TradeRadar is decision-support software, not investment advice. Trading involves risk.

Frequently asked

What is the yen carry trade?

It's the practice of borrowing yen at Japan's low interest rates, converting it into a higher-yielding currency or asset, and earning the interest-rate difference. Because it requires selling yen, it creates persistent downward pressure on the currency during calm periods.

Why does the yen strengthen when markets fall?

When risk appetite drops, carry trades are unwound. Closing them requires buying back the borrowed yen, and when everyone does this at once the yen surges. Its crisis strength is the mechanical footprint of deleveraging, not a flight to Japan.

Is the yen actually a safe haven?

The label is misleading. The yen rises in crises because it has to be repaid as leverage is withdrawn, not because investors are choosing to own it for safety. That makes it a barometer of risk-off deleveraging rather than a classic haven.

Does the yen always rise in a selloff?

No. The reaction depends on how much carry positioning exists to unwind and on Japan's rate gap versus other countries. Central-bank policy or intervention can also override the carry signal entirely.

Related in Macro & Technical

Contango vs Backwardation: What the Futures Curve Tells You

The futures curve tells you how tight a market feels before the flat price does. Here's contango vs backwardation in plain English — and what breaks the read.

Copper: the Growth Barometer They Call Dr Copper

Copper is called Dr Copper because its price reads the health of the global economy. Here's the plain-English mechanism — and what breaks the signal.

EUR/USD and Central-Bank Divergence

EUR/USD is a tug-of-war between two central banks. Here's the plain-English mechanism — how rate divergence drives the pair, and what breaks it.